We look at the advantages of borrowing money from personal contacts, to finance a property purchase and the precautions that one should take in such an arrangement

“Neither a borrower nor a lender be; for loan oft loses both itself and friend,” said Polonius, the chief counsellor to King Claudius in William Shakespeare’s tragedy Hamlet.

Let us assume, you are one of those fortunate people, who could get monetary assistance from your family members, if you were to buy a house. While this may be a tempting proposition, such home buyers often face the dilemma of whether they should utilise this option or take a home loan from a financing institution.

Thanks to the Coronavirus pandemic and its impact on the economy, home loan interest rates are at record low levels. While a slowdown in India’s residential space has resulted in a price correction in most mega markets, muted demand has ensured there is ample supply of ready-to-move-in homes in big cities. The government has also increased tax deductions on home purchases, made using housing loans.

Now, which way is the right way to go? Borrowing from your family members or friends can be a better option, provided you treat this arrangement in a professional manner and not as a personal favour.

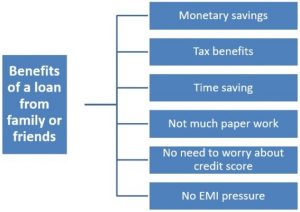

Advantages of taking a home loan from friends or family

Advantages of taking a home loan from friends or family

Monetary savings

As you may either not pay any interest or pay only a nominal interest on the borrowed capital, you will save a substantial amount. Suppose you borrow Rs 30 lakhs as a housing loan for a 20-year tenure from SBI now, at an 8% interest rate. Eventually, you will pay Rs 30.35 lakhs as interest on this amount. If the money comes from your personal contacts, this money or some portion of it could be saved and you could earn interest on it.

Tax benefits

If you get the home loan documented and pay interest on the same, you could also claim tax deductions under Section 24 of the Income Tax (IT) Act. You could annually claim Rs 2 lakhs as deductions under this section.

However, other deductions provided to borrowers under Section 80C, Section 80EE and Section 80EEA, are not available to such borrowers. It must be noted here that the lender will have to pay taxes on the interest he earns.

See also: All about home loan tax benefits

Time saving

Once you show your intent to borrow and you have someone who is willing to lend, an agreement could be drafted, to proceed with the home purchase. Banks take a lot of time to examine various documents, to gauge your creditworthiness, before they are able to tell you whether or not they would be able to lend you the money.

Not much paperwork

You will have to submit a wide variety of personal, professional and property-related documents to the lending institution, to get your home loan application approved. This need just does not arise, if you are borrowing from a friend or a family member.

No need to worry about the credit score

Among the many things that banks look at, while processing a home loan application, is the borrower’s credit score. Credit scores are assigned by credit bureaus to borrowers in India, based on the latter’s banking/payment history, on a scale of 300 to 900. In case of a poor credit score (anything below 750 is not good) you may be asked to pay a higher interest. In case the rating is much less, the bank may reject your application. When borrowing from a family member, the need to take care of this factor does not arise.

No EMI pressure

Irrespective of your financial position, you will have to pay an EMI to the lender consistently, through the course of the loan’s tenure. In case of even a single default, you may be liable to pay a penalty. In case of loss of income or some such unfortunate event, you may be allowed a moratorium period but that would have its own cost.

In the worst case scenario, the bank will have the right to repossess the property and sell it, to recover losses. These problems may not arise, if the lender is a family member. They would know your problems and support you, as you get back on your feet.

Precautions for taking home loans from friends or family

Although borrowing money from a family member to buy a house has significant benefits, it is likely to have a bearing on your personal life, if anything goes wrong with the arrangement. Hence, one should enter into this arrangement with utmost caution. Here are some points you must take care of:

Get the transaction documented

Even if you are taking this loan from your father, get it documented. It would be better, if you paid your lender some interest on the loan. Apart from the fact that this would help you earn tax benefits, this arrangement would also ensure that you do not feel guilty about taking the loan. It would also ensure that the lender does not regret his decision later.

Pay up within the stipulated time

Your lender is your personal contact but it is in your best interest that you treat this agreement as a purely financial one. Give your lender a reasonable timeline, within which you repay the loan.

FAQs

Can I claim HRA and home loan tax benefits?

A tax payer can claim HRA, as well as home loan tax benefits, in the following cases: 1) He is paying the EMI on a home loan for an under-construction project and 2) He is living in a rented property, while his own house is let out. In the second case, his income from house property will be taxable.

Can I avail of tax benefits on two home loans?

You can claim deductions within the Rs 2-lakh limit specified under section 24, on two home loans, if the properties are self-occupied. For your first home, you can also claim benefits under Section 80EE or Section 80EEA. For your second home, no deduction is available on the principal payment.

Leave A Reply